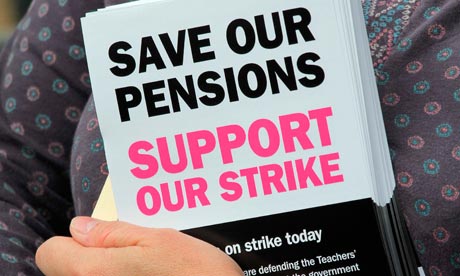

The public sector across the UK is on strike today over plans to change their pensions. The mood amongst public-sector workers will have been soured even more by the Chancellor's announcement yesterday that the cap on public-sector pay increases will be 1% per annum until 2015. If inflation stays close to its current level of 5%, that means a real pay cut of 4% per annum over the next three years!

I am tired of hearing the argument that the private sector has endured pain so now the public sector must follow suit. I have three issues with this argument. First, the private sector enjoyed most of the upside whenever things were rosy, whereas the public sector got the crumbs. Second, there is a risk-return trade-off that people who make this argument are ignoring. Private-sector workers earn a higher expected wage, but face a greater probability of pay cuts or redundancy. On the other hand, public-sector workers earn a lower expected wage, but face a lower probability of pay cuts or redundancy. Third, it was the private sector that got the economy into the mess in the first place.